Sharon Ann Murphy, "Financing Faith: Latter-day Saints and Banking in the 1830s and 1840s," in Business and Religion: The Intersection of Faith and Finance, ed. Matthew G. Godfrey and Michael Hubbard MacKay (Religious Studies Center, Brigham Young University; Salt Lake City: Deseret Book, 2019), 21–44.

I wish to thank Brigham Young University, the Latter-day Saint Church History Department, and particularly Matthew Godfrey for inviting me to speak at this year’s symposium. The sessions today have been fabulous, and everyone has been so welcoming.

When Matt first contacted me about speaking, I must admit to being more than a little surprised. I don’t study Latter-day Saint history; I don’t study the American West; I’m not a religious historian at all; and I don’t belong to The Church of Jesus Christ of Latter-day Saints. So it seemed like a somewhat odd request. Yet ironically, when he contacted me, my now nine-year-old daughter and I were reading a series of children’s books called the Great Brain that I had read and loved as a child. Partially autobiographical, the main protagonist is from a Catholic family living as a religious minority in late-nineteenth-century Utah. Although religion is not central to the story, general Latter-day Saint values as well as the local ZCMI store are recurring themes.[1] I took that as a positive sign that this Catholic girl should go give a talk at the Latter-day Saint Church History Symposium in Utah.

Now in fact, Matt did not invite me because I’m Catholic, or because I like the Great Brain books—which he also told me he loved as a kid—but because I’m a financial historian of the early American Republic. I am particularly interested in the complex interactions between financial intermediaries such as banks and life insurance companies with their clientele. I focus on understanding why financial institutions emerged, how they were marketed to and received by the public, and what the reciprocal relations were between the institutions and the community at large.

The early history of the Church of Jesus Christ, and particularly the migration of the church members first to Kirtland, Ohio, then to Missouri and Illinois, and finally to Utah, coincided with one of the most unsettled and contentious periods in the history of American banking. Thus it is perhaps not surprising that a banking controversy played a central role in the early history of the Church in Kirtland. What did surprise me, however, was the extent to which Latter-day Saint historians have dissected and debated every move made by this short-lived endeavor. Clearly one’s interpretation of the reasons for the rise and fall of this bank have much broader implications for the history of the Church of Jesus Christ more generally.

Yet the core of this debate hinges on questions whose answers lie outside the historical record: What were the intentions of the main players who created and ran the bank—known as the Kirtland Safety Society—including and perhaps especially, Joseph Smith? Were these intentions honorable, or speculative, or outright fraudulent? Were the organizers misguided in their understanding of how to run a banking institution, or did outsiders conspire to ensure its failure? And what would have happened if the bank had been able to obtain a charter from the state of Ohio? Could they have been more successful if they had played their political cards differently? Should they have sent Oliver Cowdery to petition the legislature for the charter rather than sending Orson Hyde? Could the bank have survived with this legal imprimatur from the state? In the end, did the bank fail due to poor management? the lack of a charter? bias against church members? the Panic of 1837? all of the above? none of the above?[2]

Ultimately, most of these questions are unanswerable. There is no way for us to know what would have or could have happened if the historical details had unfolded differently. It is difficult to ascertain intentionality based solely on actions. And it is particularly hard to assess blame for one bank failure in an era when bank failures were ubiquitous. Few original bank records exist (one source contends that a fire in 1837 destroyed most of these records, although the provenance of this assertion is unclear),[3] so even the detailed analyses of the bank’s operations rely largely on secondhand sources. Instead, rather than weighing in on a debate about which I could add little new insight, I want to step back and examine how the Kirtland Safety Society fits into larger questions about banks during this period. And, in particular, I want to compare the experiences of church members with money and banking in Kirtland during the late 1830s with their very different experiences a decade later in the Great Salt Lake Valley. Why were Brigham Young’s experiments with money and banking less controversial and more successful than Joseph Smith’s were?

Money and banking in the early republic were very different from what we are familiar with in the twenty-first century. Today, we more or less universally assume that money is something issued by, sanctioned by, and backed by a central government. Bitcoin and other cryptocurrencies are trying to challenge this norm by creating alternative modes of exchange outside of regulatory oversight, but these monetary exceptions demonstrate how much we have come to place our trust in the pieces of paper and coins stamped with a government seal. But the bitcoin revolution also illustrates that this norm is not the only alternative.[4]

Money has three main functions, and anything meeting these functions can serve as money. It is a medium of exchange to facilitate trade. It is a unit of account that enables you to make price comparisons between different goods and services. And it is a store of value that enables you to postpone converting your money into goods and services until a later date.[5]

Throughout history, numerous commodities have met the monetary needs of different communities. Everything from seashells, dried tobacco leaves, cocoa beans, animal skins and furs, cigarettes, and even live animals and slaves have served as money at various times and places. In most cases, a community would agree on a specific item to use as a unit of account, and then begin pricing other goods with reference to that commodity. Eventually, the government might declare that commodity to be legal tender, meaning that people would be required by law to accept that commodity as payment for goods or services.[6]

Yet even though anything can theoretically serve as money, the ideal commodity possesses several key characteristics: durability, portability, desirability, divisibility, and relative scarcity. Dried tobacco leaves were fragile and could suffer wear and tear from the process of exchange, so they were not very durable. Live animals and slaves were not easily divisible or portable, nor were they particularly durable as their value continually declined with age. Although tobacco leaves, cocoa beans, and seashells were not infinitely divisible, the value of any single leaf, bean, or shell was small enough that it could serve as an easy measure of value. Yet all three commodities could be subject to considerable supply volatility. An individual living near the ocean, for example, could potentially increase their personal money supply merely by collecting shells on the beach, while a tobacco farmer literally grew money.[7]

Since ancient times, most societies eventually turned to metals such as gold, silver, bronze, iron, or copper as the best option for commodity money. Metals are durable, almost infinitely divisible, portable (in small quantities), desirable, and relatively scarce. Yet bronze, iron, and copper were often in high demand for other uses, such as for tools and equipment. Thus, gold or silver—when available—usually became the commodity money of choice. While gold and silver were rarer than the other metals, they also had fewer competing uses. They were highly desirable yet largely only employed for ornamentation.[8]

During the colonial period, Britain mandated the use of gold or silver as money. Yet these metals were extremely rare in North America, and most British coins flowed back to the mother country in payment for imported goods. In order to have a functioning economy, the colonists were forced either to engage in barter or to use other commodities as money, such as Spanish silver coins, tobacco warehouse receipts, or wampum shells. Lacking a viable commodity to use as money, several colonial governments instead turned to paper money.[9]

Paper money can take one of two forms. Commodity-backed paper money was directly equivalent to and convertible into a specific amount of some asset, such as gold or silver. But since the lack of gold and silver was precisely the problem in the colonies, colonists instead turned to the one asset they held in abundance: land. During the eighteenth century, several colonial governments created land offices whose purpose was to issue paper money backed by real estate. Colonists could take out loans using their land as collateral, receiving paper notes of the land office in return. These notes circulated in the local economy as currency.[10]

The other type of paper money is fiat money, meaning that its value is solely based on faith in the issuing party rather than on any concrete asset. Colonial governments often issued these notes to pay military expenses, promising to accept them in payment for future taxes.[11] While commodity-backed money and fiat money are on opposite ends of the spectrum of paper money, there is actually a wide range of types of paper money that fall between these two extremes. Paper money can be issued on a fractional-reserve basis, meaning that more is printed than can be fully redeemed by the commodity in storage. The issuer predicts (or hopes) that only a portion of the notes will be returned in exchange for the commodity backing, with the remainder circulating in the economy.[12]

During the Revolutionary War, the Continental Congress was forced to print paper money without any commodity backing to pay rising military expenses. They hoped, in vain, that foreign loans, domestic loans, and contributions from individual colonies would enable them to redeem these notes. Instead, the notes depreciated rapidly in value.[13] This negative experience was fresh in the minds of the framers as they debated the Constitution. In the final document, Congress was given the exclusive power “to coin money, [and to] regulate the value thereof,” but the power to print paper money was explicitly omitted. The states, for their part, were specifically forbidden to “coin Money; emit Bills of Credit” (another term for paper money), or “make any Thing but gold and silver Coin a Tender in Payment of Debts.”[14]

Yet while this may have solved the problem of too much paper money, it did nothing to address the problem of too little gold and silver. Without a viable means of exchange, the economy of a given region could not grow. While banks emerged to serve several different functions in the economy, one of the main purposes was to provide a circulating currency beyond the limited supplies of gold and silver. Although the Constitution forbade the issuance of paper money directly by states, most states rationalized that this did not prevent them from chartering banking institutions which possessed the ability to print paper money, since this money was not designated as legal tender and received no official backing from the state.[15]

A bank is a type of financial intermediary, meaning that it facilitates the exchange of funds between creditors—people with saved money that they are willing to lend—and borrowers or debtors seeking loans. Banks accumulated these loanable funds both by selling shares of stock in the bank, and by accepting gold or silver on deposit. Both the bank’s capital stock and deposits were then available to be loaned out to borrowers seeking funds. However, rather than loaning out the precious gold and silver in its vaults, it instead issued bank notes that promised to pay back gold and silver upon redemption. Banks assumed that some of the bank notes would remain in circulation in the economy, so they issued more bank notes than they had money in their vaults to redeem—a system known as fractional-reserve banking.[16]

While most banks eventually obtained a corporate charter from the state legislature, others operated without a charter as what was known as a private bank. Several states passed legislation forbidding private banks from issuing banknotes, which often encouraged them to seek a state charter instead. But other private banks continued to operate in defiance of the laws. Many nonbank institutions, including manufacturing companies, municipalities, and individual merchants, also issued banknotes. Although technically illegal in most states, these notes circulated in the local economy when the supply of legal banknotes or gold and silver was inadequate to meet local need.[17]

As long as people had faith in the safety of the bank in question, whether chartered or not, most people preferred the convenience of banknotes over specie for making transactions. These banknotes would continue to circulate in the economy, expanding the money supply and facilitating economic transactions. Yet during times of economic distress—when specie was in greater demand to pay off debts, or when people worried about the safety of a given bank, or when debtors defaulted on their loans in large numbers—this system could unravel quickly as people withdrew their deposits and demanded specie for their banknotes.[18]

Which brings us to the 1830s. As Joseph Smith was preaching his message, gaining converts, and establishing the earliest communities of Saints, the American economy was entering another boom period. Global demand for both cotton and grain was on the rise, rapidly pushing up prices on these commodities, as well as on the land and—in the South—the slaves needed to produce them. Like Smith and his followers, Americans were heading West. And between 1830 and 1835, the number of commercial banks approximately doubled to over seven hundred institutions, all issuing banknotes and providing loans for the purchase of more land.[19]

This period likewise coincides with the infamous Bank War between President Andrew Jackson and the Second Bank of the United States. In 1832, bank president Nicholas Biddle petitioned for a renewal of the bank’s charter, which was to expire in 1836. Jackson vetoed the legislation, partially because of his hatred of Biddle (who he believed had conspired against him during the election), partially because of his distrust of paper money and the fractional-reserve banking system, and partially because of his belief that the Second Bank wielded monopoly powers that threatened the entire republican experiment of the nation by concentrating vast economic power in the hands of a small number of elite, wealthy men.[20]

Jackson was a hard-money Democrat, meaning that he believed paper money based on a fractional-reserve system was speculative gambling and that the economy should function purely on gold and silver. He not only wanted to destroy the Second Bank of the United States, but he also hoped to eradicate paper money altogether by requiring the use of specie in all government transactions, including federal land purchases.[21] While the hard-money wing of the Democratic Party had a strong voice, they were not the entirety of the Democratic electorate. A sizable proportion of Democrats still supported local banks even as they railed against the national bank. During the late 1820s and early 1830s, Democrats in Ohio regularly joined with Whigs in voting for the creation of new state-chartered banks.[22]

These banks and the banknotes they issued were critical in the rapidly developing West. Joseph Smith’s followers in Kirtland had invested in several infrastructure projects for the community during the early 1830s, including a sawmill, tannery, and printing press; they were buying up real estate to resell to newly arrived converts; and they had built a large temple. Most of this investment in the future of the town had been financed through borrowing, and the Church was heavily in debt. The incorporation of a bank to expand the local money supply was a solution pursued in many growing towns and cities, and this was the option Joseph Smith elected to adopt by the fall of 1836. Kirtland’s leaders drew up articles of incorporation for the Kirtland Safety Society Bank in November and sent representatives to the capital to petition the legislature for a charter.[23] Yet by the middle of the decade, new bank charters in Ohio were on the decline, as both intraparty fighting among Democrats and interparty fighting with Whigs blocked most new charters.[24]

While still waiting on their desired charter, the Kirtland incorporators decided to open the bank and begin operations anyway. They renamed the institution—somewhat disingenuously—the Kirtland Safety Society Anti-Banking Company, and tried to pass off the company as a nonbanking entity that happened to issue banknotes.[25] In describing these banknotes, one newspaper commentator from the Cleveland Daily Gazette stated that “previous to the word ‘bank’ in capitals, the word ‘anti’ in fine letters is inserted; and after the word ‘Bank,’ the syllable ‘ing’ is affixed in small letters also, so as to read in fact instead of Bank, ‘antiBANKing.’”[26] Although technically illegal, many other nonbanking companies throughout the country also issued banknotes. These institutions were difficult to police, and their banknotes often circulated in the local economy, providing much needed grease for the economic wheels.[27] As the Cleveland Daily Gazette article noted, “We do not object to private or company banking as a system, provided it is done upon a system and made safe.” Yet the author did question the methods employed to promote the Kirtland currency, concluding that “we consider this whole affair a deception.”[28] This author’s assessment was reprinted in newspapers throughout the Northeast.[29] Other commentators likewise asserted that “the whole is doubtless a reprehensible fraud on the public, and a violation of the laws of the state.”[30]

People based their confidence in a given banknote on their belief in the bank’s willingness and ability to redeem these notes in specie on demand. Although a corporate charter indicated that the institution met some minimum requirements set forth by the state, that charter did not ensure its success; whether or not the institution had a corporate charter was less important than its amount of specie reserves, the ratio of banknotes to these specie reserves, and the strength or weakness of its loan portfolio. Most importantly, what mattered was the public’s perception of these items. If the public believed the institution to be sound, they would willingly accept, trade, and hold onto the bank’s notes, even if the bank was operating irresponsibly in reality. If the public believed the institution to be unsound—regardless of whether or not this was true in reality—they would refuse to accept these notes (except, perhaps, at a steep discount) and would try to redeem them for specie as soon as possible. Yet a bank operating on the fractional-reserve system could not stay solvent long if their banknotes did not remain in circulation.[31] Additionally, the great number and variety of these banknotes made it easy for criminals to counterfeit notes of existing banks, to alter the face value of legitimate notes, to forge the notes of fake banks, or to continue to circulate the notes of defunct banks. As a result, people valued most highly banknotes issued by institutions close to home, about which they possessed the most knowledge and in which they could place their trust.[32]

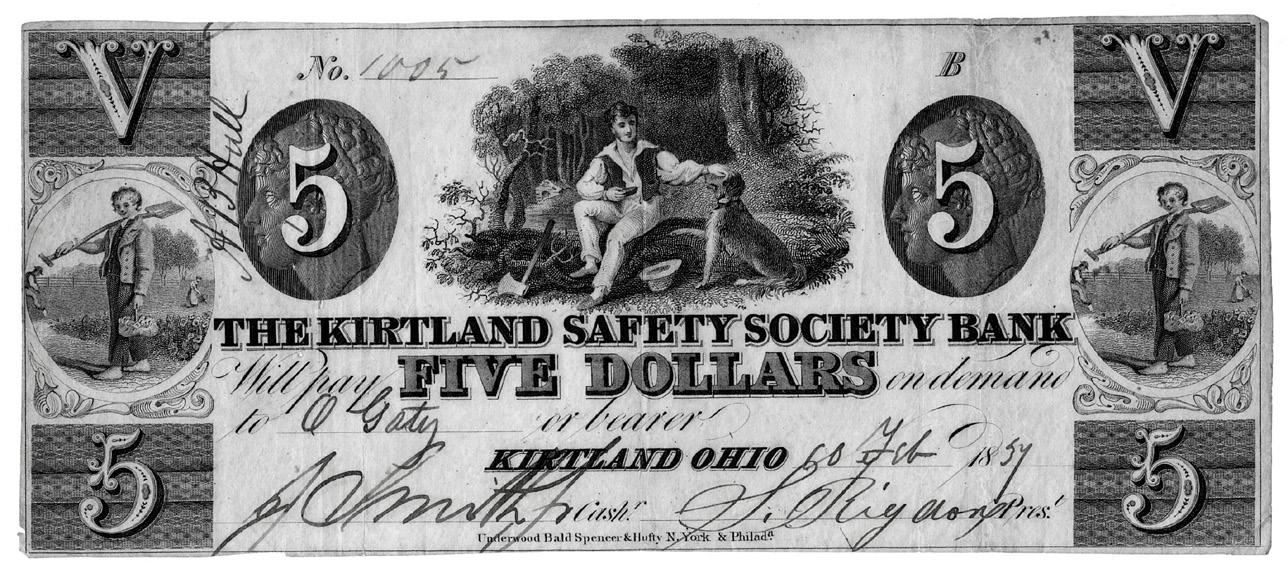

Kirtland Safety Society $5 note, 1837. Courtesy of the Church History Library.

Kirtland Safety Society $5 note, 1837. Courtesy of the Church History Library.

In issuing their banknotes during the early months of 1837, the Kirtland Safety Society was counting on the trust and confidence of the local community, especially the members of the Church. Based on the limited extant records, the bank likely lacked adequate specie reserves to function. Most banks obtained the majority of their loanable funds by selling stock, but it appears that subscribers to the Kirtland Safety Society provided very little specie in exchange for their stock. Instead, they paid the first installment of the price—which was already a small fraction of the stock’s full value—either in banknotes of other institutions, or by putting up their real estate as collateral.[33] But again, what they really had in their vaults mattered less than people’s confidence in their continued existence and their ability to redeem banknotes on demand.

Critics were quick to question the soundness of the Kirtland Safety Society notes. People from Ohio, New York, New Jersey, and Connecticut all read in their local newspapers: “As far as we learn there is no property bound for their redemption, no coin on hand to redeem them with, and no responsible individuals whose honesty is pledged for their payment.” Rather than having backing in some concrete asset, the author concluded that the notes “seem to rest upon a spiritual basis.”[34] Others directly challenged the wisdom of mixing religion and economics. As one Massachusetts newspaper commented, “When the devout worshippers of the Golden Bible give themselves up to the delusion of paper money, what can be expected of the bank publicans, and shaving sinners, among the unbelievers?”[35]\

By mid-February, newspapers from Ohio to New York were already reporting that the Kirtland Safety Society had “stopped payment” on its banknotes, although they added somewhat sarcastically that “The Ohio City Argus says, however, that Jo Smith will pay in real estate!”[36] Other newspapers rebutted these claims, declaring instead that “the Kirtland Safety Fund Bank (Mormon Bank) has not stopped payment, but redeems its notes with specie.”[37] Regardless of which report was more accurate, these competing accounts could hardly inspire confidence in the public. Local Ohio newspapers such as the Canton Repository and the Scioto Gazette of Chillicothe consequently advised: “We caution our readers against taking this paper.”[38]

Whether it was because they lacked a charter, or because people suspected that their specie reserves were too low, or because people were wary of any brand-new banking institutions, or because nonmembers questioned the close relationship between the bank and the Church, public confidence in the Kirtland Safety Society was inconsistent from the beginning. While debtors flocked to the bank to obtain loans in the form of banknotes that circulated in the immediate community, others questioned the ability of the bank to redeem these notes on demand. In particular, Kirtland residents had difficulty using these notes for the purchase of goods outside the immediate area, as many merchants and banks beyond Kirtland refused to accept them.[39] As the Maysville Monitor out of Kentucky reported in May: “A company of fellows on their way to Illinois and Missouri, stopped in Maysville and attempted to palm upon our good citizens a lot of Joe Smith’s currency. . . . It was ‘no go,’ however, for the Maysvillians were too smart to receive Mormon Money.”[40] While it is difficult to tell whether this author was most concerned about the soundness of the banknotes or the religious provenance of the currency, readers got the clear message that the money was not acceptable.

It is impossible to know whether or not the Kirtland Safety Society would eventually have been able to build the public confidence they would need to sustain operations since the Panic of 1837 hit during this early, experimental period of the bank’s existence. High cotton prices during the 1830s—a major component of the speculative growth—encouraged not only an increase in American supply but also growth in global competition from places like India. The growing supply outpaced demand, which led to falling cotton prices by 1837, thus depressing land values that had risen sky-high based on speculation. Beginning in the critical port city of New Orleans, cotton merchants began to fail.[41]

By May 1837, New York City banks had suspended specie payments, instigating a panic that spread throughout the nation. Businesses of all kinds failed. Unemployment rose. Prices declined. Land values plummeted. Debtors defaulted on their loans, contracting the money supply and reducing much-needed specie reserves. People questioned which banking institutions were safe and reliable, and which were irresponsible with their funds or even downright fraudulent. Many people opted to redeem their banknotes immediately for specie, just in case their bank was one of the unsound ones. But by this very action of cashing in banknotes or removing deposits, they precipitated the event they feared—draining specie reserves and forcing the bank to close its doors.[42] Newly established banking institutions like the Kirtland Safety Society were often the first to fail, mainly because they had had the least time to establish a positive reputation for soundness within the community. By the fall of 1837, the Kirtland Safety Society Anti-Banking Company had closed its doors.[43]

With the failure of the Kirtland Bank, Joseph Smith and his followers appear to have abandoned the idea of using banks to promote economic development and alleviate their debt problems. During their subsequent stays in Missouri and Illinois, there was no attempt to charter a new banking institution for the Saints. In order to facilitate exchange, the leaders in Nauvoo instead issued $1 notes known as scrip.[44] Scrip was pure fiat currency with no commodity backing and no legal standing. It was issued outside of the banking system and only intended to circulate in the local economy to meet the immediate, day-to-day needs of exchange.[45] However, when the Church members left Illinois in the mid-1840s, heading West to establish an independent settlement free from the persecution they suffered in Missouri and Illinois, more pressing issues of money and banking would soon reemerge.

While the majority of Saints migrated from Illinois with Brigham Young into the Great Salt Lake Valley, a smaller group of members from the Northeast went by ship around South America to California. During the course of this journey, war had broken out between the United States and Mexico. By the time this small group arrived in San Francisco Bay, the region was already occupied by the United States. Another small band of Church members who had fought for the United States during the Mexican-American War soon joined the San Francisco group.[46] These groups eventually settled nearby in Sutter’s Fort, working for a man named Captain John Sutter. Sutter had little cash to pay the workers, but gladly paid them in kind—with food, seeds, tools, and livestock. Many of these supplies were then sent to the main settlement of Saints in the Great Salt Lake Valley.[47]

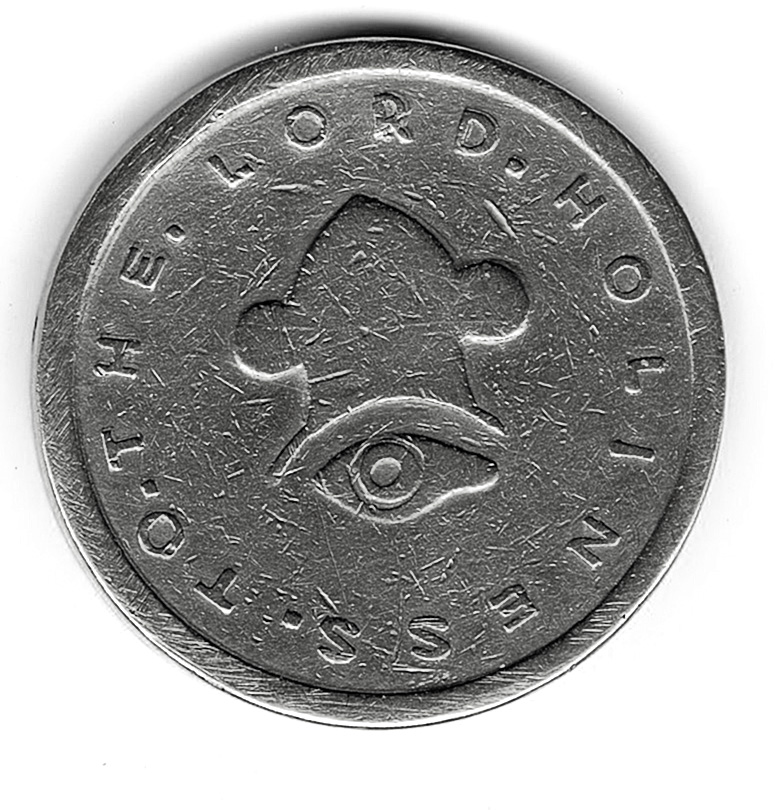

It was here at Sutter’s Mill that gold was first discovered in 1848, ushering in the California gold rush. Now, in addition to food, supplies, and livestock, gold dust also flowed into the Great Salt Lake Valley.[48] Brigham Young immediately decided to coin money for the community using this gold dust.[49] These coins, minted in several different denominations, were stamped on one side with an emblem of the priesthood and the words “Holiness to the Lord.” On the reverse was a picture of two clasped hands symbolizing friendship with the words “Pure Gold” and the coin’s value.[50] The minting of these coins violated the United States Constitution, which reserved the minting of coins exclusively to the federal government.[51] Although the Great Salt Lake Valley had been outside the territorial limits of the United States when the Saints first arrived, Mexico ceded the land to the United States in the Treaty of Guadalupe Hidalgo, which ended the Mexican-American War and placed the Church once again under the jurisdiction of the United States.[52]

Front and back of a $10 Utah gold coin, 1849. Courtesy of the Church History Library.

Front and back of a $10 Utah gold coin, 1849. Courtesy of the Church History Library.

Problems with the minting process, however, limited the number of coins initially created.[53] Additionally, it would have been difficult to mint small denomination gold coins because they would have been much too tiny to handle. This is one of the reasons why the United States remained on a bimetallic standard for most of the nineteenth century—small denomination coins could be minted with the less-valued silver and large denomination coins with gold. To address this need for small denomination currency, the Saints in Utah began printing paper money, redeemable in gold dust. By January 1849, they were issuing one-dollar, three-dollar, and five-dollar notes. Later in the month, they started printing fifty-cent notes as well.[54]

Somewhat ironically, the Salt Lake high council also passed a resolution permitting the use of the defunct Kirtland Safety Society banknotes as valid currency.[55] By the end of the year, they had resumed minting coins, supplementing these banknotes with gold coins valued at $2.50, $5, $10, and $20.[56] Overall, during this early period from 1847 to 1850, the Church treasury printed an estimated $10,000 in gold-backed notes—which were mainly intended to circulate within the local community—and another $70,000 in gold coins, mostly for external trade. Although they initially intended the paper money to be 100 percent backed by gold, in reality these banknotes were issued on a fractional-reserve basis.[57]

Unlike the experience of the Kirtland Bank, the paper money and gold coins produced in Utah were neither controversial nor problematic. Although the coins were illegal, they still had intrinsic value. Merchants and traders readily accepted this currency, since it could be easily melted down and sold back East. But even the paper money hardly raised any eyebrows. Both the Kirtland Safety Society notes from the 1830s and the Utah notes from the 1840s were promises to pay in gold. They differed not in substance but in the public’s belief about their long-term value.[58]

In Kirtland, the public questioned whether or not the society had adequate gold supplies to redeem its notes. Certainly, the general scarcity of gold and silver in the 1830s contributed to this skepticism. In Utah, on the other hand, where both real and exaggerated stories of gold strikes in California circulated throughout the population, supported by concrete evidence whenever migrants arrived in town with their gold dust, it was much easier for the public to believe that the Church possessed adequate gold reserves to redeem these notes. In effect, rather than needing to obtain scarce gold and silver through trade (as had been the case in Ohio), Church members could expand the local money supply by sending groups of Saints into California in search of gold to bring back to the community.

The 1830s and 1840s were a period of experimentation with money and banking in the United States. The experience of the Saints during this time highlights some of the most important elements of this financial history. First, it was difficult for any group—no matter how isolated geographically or ideologically—to survive without something to serve the functions of money. While many commodities or even fiat paper money might have been able to meet the internal needs of a closed community, interactions with the outside world required money that could generate wider public trust. In Kirtland, Ohio, in 1836—where gold and silver were scarce, land speculation was widespread, and the bank was dubbed an “anti-banking company”—it was difficult to generate public trust in an untested banking institution. Its failure during the Panic of 1837, while not inevitable, was still highly likely in this climate. Survival would have required the local community members to be both willing and able to contribute significant liquid funds to sustain it during the downturn. But a lack of liquid funds was exactly why they had decided to charter a bank in the first place.

The communal need for some form of money was also present in the Great Salt Lake Valley in the late 1840s, yet the material conditions were much different. Rather than a scarcity of gold and silver, the California gold rush ushered in the perception of easy money. Ultimately, it was this perception that mattered. The Saints could trade paper money internally—even the old bills of the Kirtland Safety Society—secure in the belief that they could be redeemed for gold on demand. They did not need any external validation of this paper money. On the other hand, their ability to mint gold coins guaranteed the acceptance of their money with outsiders. No one cared what government claimed sovereignty over the coins, since they could always be melted down and reminted.

Ultimately, engaging in monetary exchange—whether through the use of gold and silver, paper money, or bitcoins—is an act of faith. But as the experiences of Church members in Kirtland and Utah demonstrate, monetary faith often requires material evidence not necessary for religious faith.

Notes

[1] John D. Fitzgerald, The Great Brain (New York City: Dial Books, 1969).

[2] Roger D. Launius, “The Latter Day Saints in Ohio: Writing the History of Mormonism’s Middle Period,” John Whitmer Historical Association Journal 30, no. 4 (1996): 33–36, 52–53; Dale W. Adams, “Chartering the Kirtland Bank,” BYU Studies 23, no. 4 (Fall 1983): 467; Mark Lyman Staker, Hearken, O Ye People: The Historical Setting for Joseph Smith’s Ohio Revelations (Salt Lake City: Greg Kofford Books, 2009), 463–501; Dean A. Dudley, “Bank Born of Revelation: The Kirtland Safety Society Anti-Banking Company,” Journal of Economic History 30, no. 4 (December 1970): 848; Marvin S. Hill, C. Keith Rooker, and Larry T. Wimmer, “The Kirtland Economy Revisited: A Market Critique of Sectarian Economics,” BYU Studies 17, No. 4 (Summer 1977): 392–94, 437–43, 459–60.

[3] Dudley, “Bank Born of Revelation,” 851.

[4] Clive Thompson, “What the Founding Fathers’ Money Problems Can Teach Us about Bitcoin,” Smithsonian Magazine, April 2018.

[5] Edwin J. Perkins, American Public Finance and Financial Services, 1700–1815 (Columbus: Ohio State University Press, 1994), 13; Gary M. Walton and Hugh Rockoff, History of the American Economy (New York: Dryden Press, 1994), 73; Sharon Ann Murphy, Other People’s Money: How Banking Worked in the Early American Republic (Baltimore: The Johns Hopkins University Press, 2017), 12–15.

[6] John Kenneth Galbraith, Money: Whence It Came, Where It Went (Boston: Houghton Mifflin, 1975), 7; Walton and Rockoff, History of the American Economy, 74; Murphy, Other People’s Money, 15.

[7] Howard Bodenhorn, State Banking in Early America: A New Economic History (New York: Oxford University Press, 2003), 130–31; Galbraith, Money: Whence It Came, 8; Murphy, Other People’s Money, 15–16.

[8] Perkins, American Public Finance, 16–17; Galbraith, Money: Whence It Came, 8–9; Murphy, Other People’s Money, 16–17.

[9] Perkins, American Public Finance, 22–27, 39–46; Galbraith, Money: Whence It Came, 47–52; Murphy, Other People’s Money, 17.

[10] Perkins, American Public Finance, 41, 44–46; Galbraith, Money: Whence It Came, 46–47; Murphy, Other People’s Money, 17–20.

[11] Perkins, American Public Finance, 29–31, 42–43; Galbraith, Money: Whence It Came, 51–55; Murphy, Other People’s Money, 19–20.

[12] Perkins, American Public Finance, 119–21; Walton and Rockoff, History of the American Economy, 254–57; Murphy, Other People’s Money, 20.

[13] Perkins, American Public Finance, 85–105; Galbraith, Money: Whence It Came, 58–59; Walton and Rockoff, History of the American Economy, 135–36; Murphy, Other People’s Money, 20–25.

[14] Constitution of the United States, article I, sections 8 and 10; Walton and Rockoff, History of the American Economy, 136–37; Murphy, Other People’s Money, 30–32.

[15] Perkins, American Public Finance, 266–81; Galbraith, Money: Whence It Came, 70–71; Murphy, Other People’s Money, 56–57.

[16] John Lauritz Larson, The Market Revolution in America: Liberty, Ambition, and the Eclipse of the Common Good (New York: Cambridge University Press, 2010), 26; Perkins, American Public Finance, American Public Finance, 118–23; Walton and Rockoff, History of the American Economy, 254–57; Murphy, Other People’s Money, 42–49.

[17] Richard Sylla, “Forgotten Men of Money: Private Bankers in Early U.S. History,” Journal of Economic History 36, no. 1(March 1976): 173–88; Larson, Market Revolution in America, 26; Murphy, Other People’s Money, 53–54, 62–63.

[18] Larson, Market Revolution in America, 39–45; Murphy, Other People’s Money, 77–78.

[19] Jessica M. Lepler, The Many Panics of 1837: People, Politics, and the Creation of a Transatlantic Financial Crisis (Cambridge University Press, 2013), 8–42; Larson, Market Revolution in America, 92; Murphy, Other People’s Money, 99–100.

[20] Stephen Mihm, “The Fog of War: Jackson, Biddle, and the Destruction of the Bank of the United States,” in A Companion to the Era of Andrew Jackson, ed. Sean Patrick Adams (Hoboken, NJ: Wiley-Blackwell, 2013), 348–49, 357–61; Lepler, Many Panics of 1837, 20–23; Murphy, Other People’s Money, 96–99.

[21] Lepler, Many Panics of 1837, 19–20; Mihm, “Fog of War,” 355–56; Murphy, Other People’s Money, 100–102.

[22] William Gerald Shade, Banks or No Banks: The Money Issue in Western Politics, 1832–1865 (Detroit: Wayne State University Press, 1972), 22–28; Murphy, Other People’s Money, 107–10.

[23] Brent M. Rogers et al., eds., Documents, Volume 5: October 1835–January 1838, vol. 5 of the Documents series of The Joseph Smith Papers, ed. Ronald K. Esplin, Matthew J. Grow, and Matthew C. Godfrey (Salt Lake City: Church Historian’s Press, 2017), 285–86, 293, 299–306; Staker, Hearken, O Ye People, 448–52, 463–66; Adams, “Kirtland Bank,” 468–72; Dudley, “Bank Born of Revelation,” 849–50; Hill, Rooker, and Wimmer, “Kirtland Economy Revisited,” 430–34.

[24] Shade, Banks or No Banks, 79–83; Adams, “Kirtland Bank,” 473–75; Staker, Hearken, O Ye People, 467–71.

[25] Rogers et al., JSP, D5:324–31; Adams, “Kirtland Bank,” 475; Dudley, “Bank Born of Revelation,” 851; Hill, Rooker, and Wimmer, “Kirtland Economy Revisited,” 434; Staker, Hearken, O Ye People, 476–77.

[26] “A New Revelation—Mormon Money,” Cleveland Daily Gazette, 12 January 1837, 2.

[27] Dale W. Adams, “Grandison Newell’s Obsession,” Journal of Mormon History 30, no. 1 (Spring 2004): 185; Staker, Hearken, O Ye People, 474–75.

[28] “A New Revelation—Mormon Money,” 2.

[29] “New Revelation,” Newark Daily Advertiser, 1 February 1837, 2; “New Revelation,” New-York American, 3 February 1837, 4; “New Revelation,” Connecticut Courant, 4 February 1837, 2.

[30] “Mormon Money,” Boston Courier, 6 February 1837, 1.

[31] Murphy, Other People’s Money, 56–60.

[32] Stephen Mihm, A Nation of Counterfeiters: Capitalists, Con Men, and the Making of the United States (Boston: Harvard University Press, 2007), 1–19; Murphy, Other People’s Money, 60–63.

[33] Rogers et al., JSP, D5:288–90, 302; Adams, “Kirtland Bank,” 476–77; Dudley, “Bank Born of Revelation,” 851–52; Hill, Rooker, and Wimmer, “Kirtland Economy Revisited,” 449–51; Staker, Hearken, O Ye People, 478–80.

[34] “A New Revelation—Mormon Money,” 2; “New Revelation,” Newark Daily Advertiser, 1 February 1837, 2; “New Revelation,” New-York American, 3 February 1837, 4; “New Revelation,” Connecticut Courant, 4 February 1837, 2.

[35] “Mormon Money,” Barre Gazette (MA), 17 February 1837, 2.

[36] “Mormon Bank,” Evening Post (NY), 8 February 1837, 2; “Mormon Bank,” Daily Pennsylvanian, 9 February 1837, 2; “Mormon Bank,” Commercial Advertiser (NY), 10 February 1837, 1; “Mormon Bank,” Columbian Register (CT), 11 February 1837, 3; “Mormon Bank,” Newburyport Herald (MA), 14 February 1837, 2; “Mormon Bank,” New-York Spectator, 14 February 1837, 4; Boston Traveler, 17 February 1837, 2; and Vermont Watchman, 21 February 1837, 3. See also Saratoga Sentinel (NY), 21 February 1837, 3.

[37] “Bank of Monroe,” Evening Post (NY), 16 February 1837, 2. See also, “Bank of Monroe,” Albany Argus (NY), 17 February 1837, 3.

[38] “Mormon Bank,” Scioto Gazette (OH), 15 February 1837, 3.

[39] Rogers et al., JSP, D5:287–88, 331–40; Dudley, “Bank Born of Revelation,” 852–53; Hill, Rooker, and Wimmer, “Kirtland Economy Revisited,” 434–36; Staker, Hearken, O Ye People, 481–91.

[40] “A ‘Better Currency,’” Philadelphia Inquirer, 5 May 1837, 2; and “Mormon Money,” Columbian Centinel (MA), 6 May 1837, 4.

[41] Lepler, Many Panics of 1837, 43–66; Murphy, Other People’s Money, 99–101.

[42] Lepler, Many Panics of 1837, 123–56; Larson, Market Revolution in America, 92–96; Murphy, Other People’s Money, 101–2.

[43] Dudley, “Bank Born of Revelation,” 853; Launius, “Latter Day Saints in Ohio,” 52.

[44] Richard Neitzel Holzapfel and T. Jeffery Cottle, A Window to the Past: A Photographic Panorama of Early Church History and the Doctrine and Covenants (Salt Lake City: Bookcraft, 1993), 29.

[45] Murphy, Other People’s Money, 62–63.

[46] Kenneth Owens, “Far from Zion: The Frayed Ties between California’s Gold Rush Saints and LDS President Brigham Young,” California History 89, no. 4 (2012): 5–12; Walter Nugent, “Tanner Lecture: The Mormons and America’s Empires,” Journal of Mormon History 36, no. 2 (Spring 2010): 6–9.

[47] J. Kenneth Davies, “Mormons and California Gold,” Journal of Mormon History 7 (1980): 84; Owens, “Far from Zion,” 12–14.

[48] Larry Schweikart and Lynne Pierson Doti, “From Hard Money to Branch Banking: California Banking in the Gold-Rush Economy,” California History 77, no. 4 (Winter 1998/

[49] Davies, “Mormons and California Gold,” 90; Schindler, In Another Time, 46; Stanley, “First Utah Coins,” 244.

[50] Schindler, In Another Time, 48; Stanley, “First Utah Coins,” 244–45.

[51] Constitution of the United States, article I, sections 8 and 10.

[52] Nugent, “Mormons and America’s Empires,” 4–5, 10.

[53] Davies, “Mormons and California Gold,” 90–92; Stanley, “First Utah Coins,” 244.

[54] Schindler, In Another Time, 46; Stanley, “First Utah Coins,” 245.

[55] Schindler, In Another Time, 46; Stanley, “First Utah Coins,” 245.

[56] Stanley, “First Utah Coins,” 245.

[57] Leonard J. Arrington, “Banking Enterprises in Utah, 1847–1880,” Business History Review 29, no. 4 (December 1955): 313.

[58] Schindler, In Another Time, 46.